Print's luxury future

Magazines aren't dead, they just need to get used to being a luxury

“Print is dead…”. God, that phrase annoys me. The decline of one or two sectors of the magazine industry, and the generalised replacement of print newspaper circulation with digital subscriptions, has been taken to mean that the entire sector is in some kind of terminal decline.

That is emphatically not the case. It’s a cliché to say that television didn’t kill radio - but it didn’t, just as digital won’t kill print.

Now before you think me some kind of reactionary throwback, I’m not suggesting that print is on the cusp of some new golden age where it throws off the years of decline and ascends to new heights.

Instead, I’m suggesting that it’s approaching a critical point in its transition from being a mass-market product to a niche-focused, more luxury product.

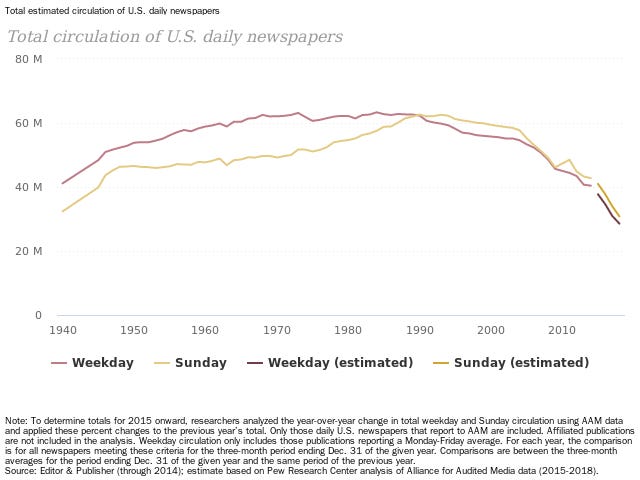

For most of the period since WW2, print periodical publishing was dominated by two sectors - daily newspapers and women’s magazines. This chart, taken from Pew Research Center’s Newspaper Fact Sheet, shows the problem :

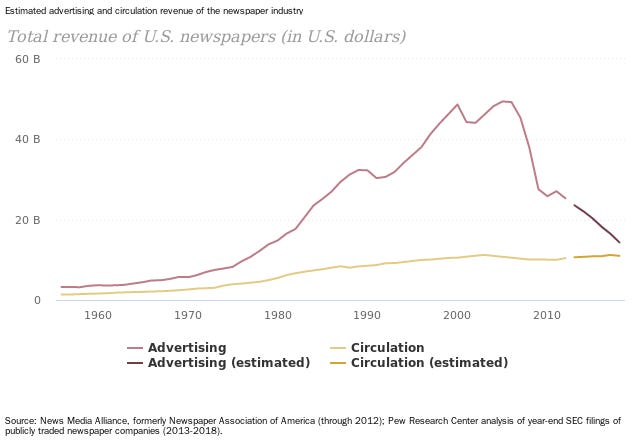

Circulation for US dailies is now below where it was in 1940. The picture for revenue shows a similar story (although there’s more of a case to suggest that 1980-2010 represented a one-off, ad-fuelled bubble) :

I don’t have a comparable graph for magazines but here’s some basic numbers that illustrate the point, comparing the circulation of two weekly women’s / entertainment titles in the UK from 2012 to today :

I picked those more or less at random, I could have picked pretty much any title in those categories. Compare those figures with specialist titles, such as BBC History magazine or Classic Rock magazine, and you won’t find a decline anywhere near as sharp.

In other words, niche titles have ridden out the generalised shift to digital media better than more mass-market titles. Niche titles have another inherent advantage in that they are able to charge higher cover prices than mass titles.

If you accept that for most mass-market media providing essentially undifferentiated content (not all of them do this but most do), their future is “a race to the bottom” which they can never hope to win in the face of pure digital competitors unburdened by print’s legacy overhead, then I would suggest that print’s future has the following characteristics :

Lower Frequency - historically, tactics around print frequency were essentially drive by two factors : i) newsstand competition - think of that “13th issue” for monthlies that could drive a few thousand more to the bottom line; ii) topicality - the dependency that some titles had on remaining as ‘fresh’ as possible in the pre-internet era, particularly in the face of newspapers that weren’t as diverse in their content offerings as they are today. Newsstand is declining rapidly in importance - with Covid accelerating this trend - meaning that publishers can be more fluid with frequency. Publishing 8 or 10 issues a year - which once drove distributors crazy - is much easier to do when the majority of your sales are direct to consumers;

More Content - this may seem counter-intuitive in the face of many publishers’ drive to cut costs. But the key here is to improve the overall perception of value for consumers. You can get away with fewer drops (see above), providing each drop lingers longer in the home and has a higher perceived value. More content - and the increased pagination that this requires - is an inevitable, and necessary, step to take in achieving this. Compare and contrast an issue of, say, Rolling Stone magazine in its pre- and post-relaunch iterations and you will see immediately what I mean. Look also at indie magazines like Delayed Gratification or The Road Rat, where page counts in the hundreds are the norm.

Higher Price - obviously, you’ve got to pay for all that extra content (and all those extra pages) somehow. The good news is that the cover price trend in print is relentlessly upwards. The reality is that for many years, we underpriced our products dramatically. A magazine charging £4.99 ($7.00) - which in London is less than the price of a pint of beer - is telling its audience everything they need to know about perceived value. High quality magazines now are successfully pushing prices above £10 ($14.00) or even £15 ($21.00) in some cases, which changes the economics of print dynamically.

Clear Positioning (preferably in a niche) - my personal view is that the days of the mass market magazine are drawing to a close and we are at the dawn of the niche magazine. In some markets - the UK and other parts of Europe - the power of niches has been understood for a while but it is only in the digital age - where the “long tail” approach has revealed markets in every gaps possible - that these are starting to become the centre of media businesses and not the periphery. Print’s future lies in finding and building on niches, identifying and engaging with specialist (sometimes highly specialist) audiences, ideally as part of a multi-platform strategy.

More Direct Sales - let’s be honest, newsstand is a necessary pain in the arse, but a pain in the arse nonetheless. Retailers are terrible at displaying and marketing magazines correctly and the supply chain is a nightmare. On average, you end up printing at least 2 copies for every 1 that you sell (and in some cases more than that) - an economic and environmental hole that the industry needs to climb out of. Selling directly to your consumers via a subscription, and doing so profitably (unlike the older US model of piling ‘em high and selling ‘em cheap to deliver an ad-driven circulation number) offers a real alternative to newsstand. Consumers, increasingly used to e-commerce, are comfortable buying magazines this way too, something publishers should exploit.

Less Advertising - smart independent publishers build the business plans for their magazines without advertising. They know that it will take many years from launch - if at all - before a smaller title hits advertisers’ radars. Now, I’m not saying that more established players should throw advertising out the window completely. Instead, publishers should see if they can build a publishing model that works on circulation - and other revenue streams such as digital paid content and e-commerce - alone, and view advertising as a bonus. That way, the business will be much better insulated from the inevitable peaks and troughs of the advertising market.

And, for some :

Rejecting digital in favour of strong print journalism - the standard-bearer for this approach is the UK’s news and current affairs title Private Eye. Having rejected, in the early days of the internet, the need to put content on their website for free (for the good reason that they couldn’t see how they would make money out of it), their print edition continues to boom. Not everyone can or should adopt this approach but it’s comforting to know that strong, unique journalism can still drive print success.

This is a very quick overview of a complex subject but hopefully the central premise - that print has an exciting place in the media mix of tomorrow - still holds.

Print is not dead, it’s merely a caterpillar that has taken a few hundred years to turn into a butterfly…