The customer is king again

How media moved from worshipping the advertiser to loving the customer

I never intended that this first post be all about the New York Times but having started looking at their data in support of my opening point, I disappeared down a rabbit hole of analysis.

My point was going to be that nothing illustrates the change in the media industry - which for some companies is one they’ve already been through and for others is a journey they’ve yet to begin in earnest - better than the NYT in recent years.

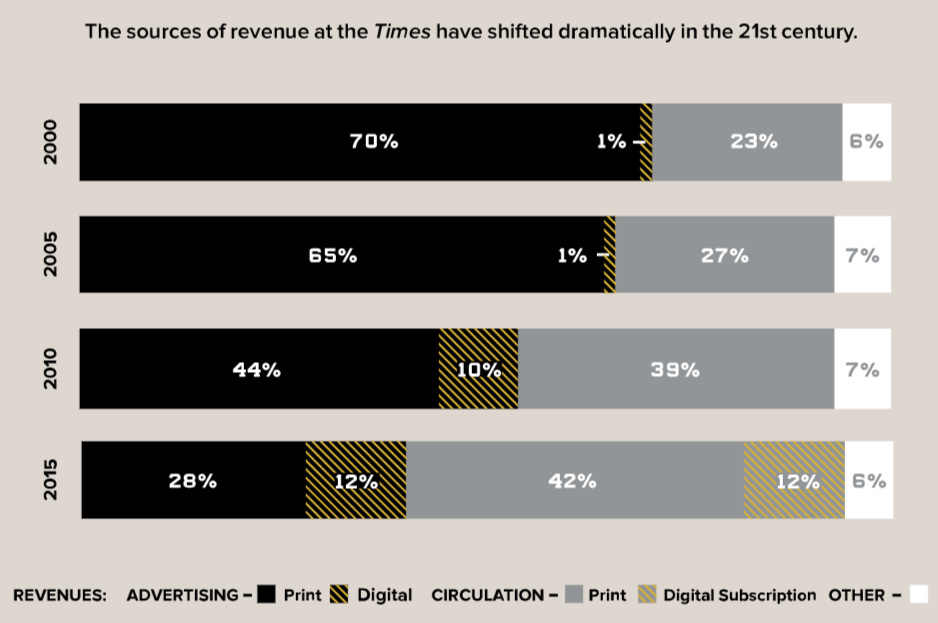

This graph, which was originally published in one of the NYT’s own reports, was widely shared when it first came out :

Even in 2015, the balance had already shifted away from advertising towards circulation - putting the reader first.

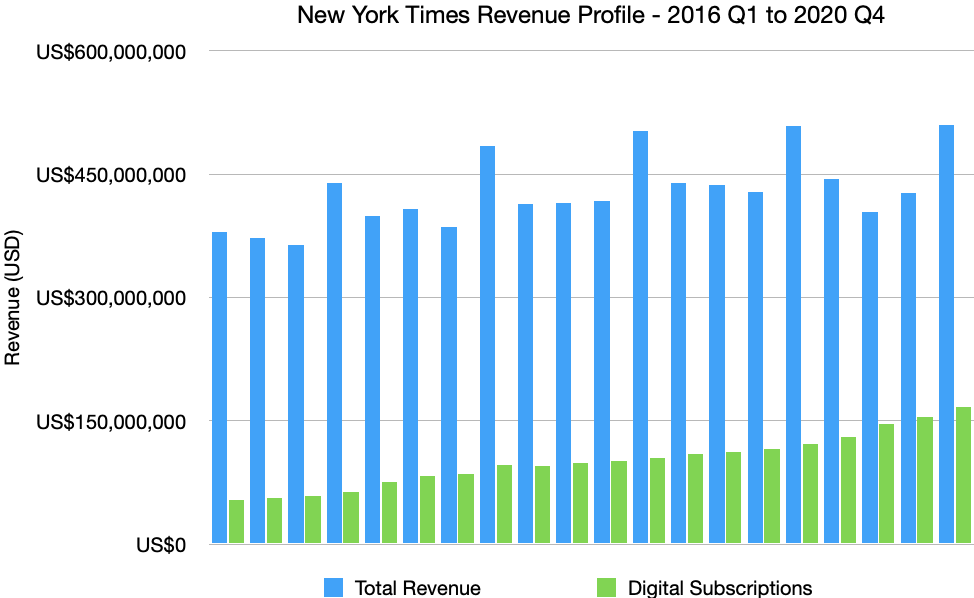

Using data sourced from a combination of FIPP’s Digital Subscriptions Snapshot (full disclosure : I work for FIPP, this report sits in our members-only area, so you’ll have to pay to see it) and from the NYT’s own investor relations pages, you can build a picture of the story since 2015. Firstly, look at the revenue picture in overall terms :

I’ve left the exact dates of this to focus on the revenue profile but this shows NYT revenue from Q1 of 2016 to Q4 of 2020, a 5-year period in which everything changed for them.

Two things are immediately obvious :

Overall, the business is on an upward curve in terms of total revenue, in fact it grew by 15% in this period - meaning that for NYT, the shift in revenue streams didn’t come at the cost of growing the business overall

Secondly, it’s clear that the green bars, representing digital subscriptions revenue, have grown by far more than the total - this grew at a staggering 157% over the same period!

Not shown on this graph is the total advertising revenue but I can tell you that it went from $185m in Q4 of 2016 (the fourth quarter always being NYT’s biggest) to $139m in Q4 2020, in other words a 25% decline.

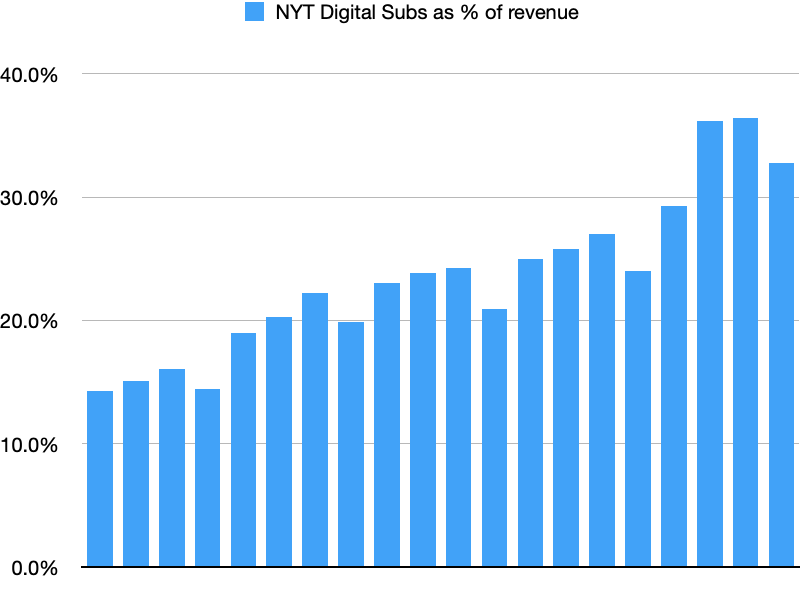

When you look at what percentage of NYT’s revenue is accounted for by digital subscriptions, the true picture becomes clear :

(this graph is over the same period, Q1 2016 to Q4 2020). Digital subscriptions have gone from being about 15% of total revenue - interesting but no more important than a few other things - to 33% in Q4 2020. If you go back one quarter, where the impact of holiday-season advertising is stripped out, the share is 36%! In fact, in Q3 2020, digital subscriptions were the single biggest source of revenue for the paper.

With no sign that the growth of digital subscriptions slowing, even allowing for the end of the ‘Trump bump’, it’s clear that this new revenue stream is not only going to cement its place as the thing Arthur Sulzberger wakes up in the morning thinking about but it will stretch away and become waaaay more important than any of the others.

So why is this important? A lot of people tell me “that’s great, but there’s only one New York Times…”

It’s important because it’s symbolic of a shift in our industry’s finances that is not only inevitable but necessary. The shift from an indirect relationship with our consumers through advertising to a direct one through digital subscriptions, e-commerce, live events and membership.

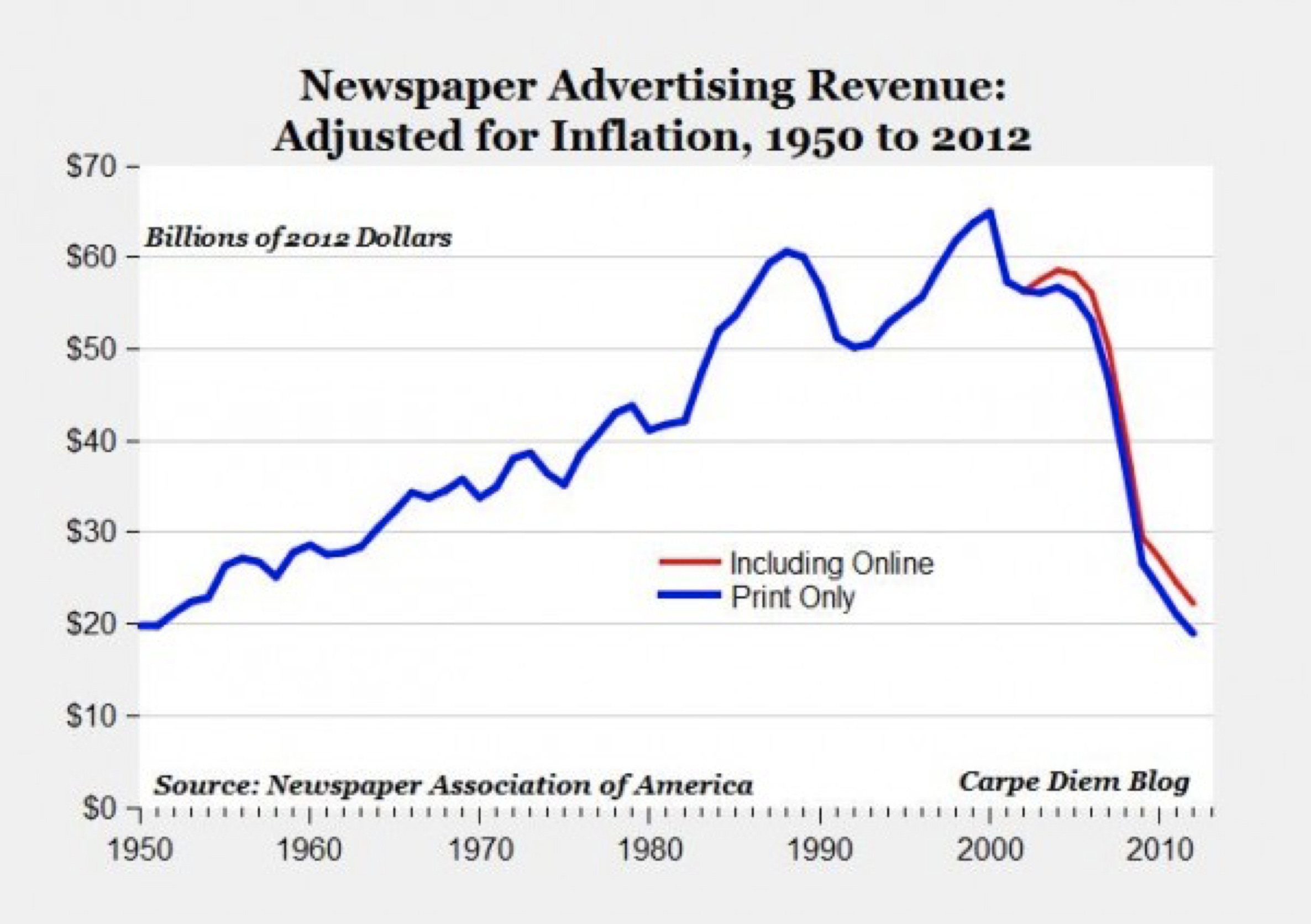

The shift all started here :

This was taken from the organisation that’s now called the New Media Alliance and it shows the issue as plainly as you could want.

In the last 20 years or so, for American newspapers, all of the gains made in advertising revenue since WW2 have been wiped out by the internet. I’ll say that again - ALL of the gains, even adjusted for inflation, have gone! Whoof! Vanished! (We all know where they’ve gone, but that’s a subject for another time…)

And for newspapers, you can substitute magazines too. And for American, you can substitute any country you like. (TV and radio are a different story, we’ll come on to them in a future update).

This was and remains an existential crisis for the business, easily demonstrated by the approximately 1,800 newspapers that have closed in the US since 2004. Many towns and cities in America now have no local news outlet at all.

So if you’re a media business, what did that mean? You could sit still, cut costs and hope the ads come back (there are plenty of businesses following this strategy btw, including at least one I worked at where the internet was described as “a fad”).

Or, if you want to stay in business, and crucially if you want to overturn another cliché : “you can’t cut your way to growth”, you look for new sources of revenue. And the key here is the reader.

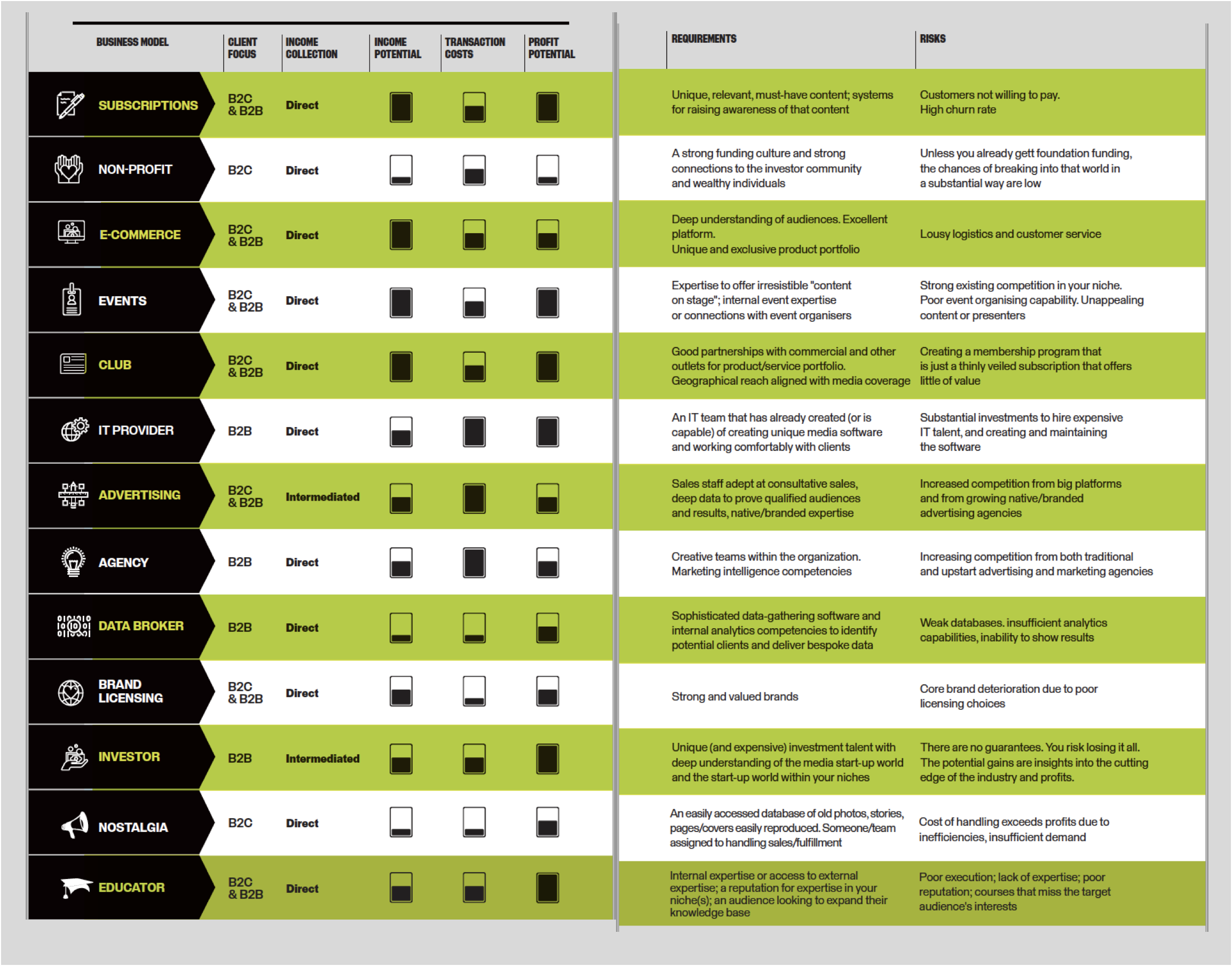

Innovation Media Consulting, who work with FIPP in producing their annual Innovation in Media World Report (sorry, yes you’ll have to join FIPP to see that too - they won’t all be FIPP links, I promise…), have sought to contextualise this by identifying all the different sources of revenue that media companies can now target, as they look to replace the lost advertising revenue :

(For a full explanation of each of these, you’ll need to buy the report)

The key column here is “Income Collection” - fully 11 of the 13 business models outlined are “Direct”, meaning they involve a direct relationship between the media business and the end customer. Strip out the ones that are B2B only and you are left with 7 that rely on a brand building a direct, transactional relationship with a consumer.

There are many different aspects to this journey, and I’ll touch on all of them in forthcoming posts - the digital “maze” where every exit is blocked by either Google or Facebook; what the ongoing efforts to regulate them might mean for this picture; how sustainability should play a part in your thinking about revenue streams; the “buy or build” debate in technology; the new importance of first party data as cookies die a death; and so on… - but the fundamental is this : for 70 years we put the advertiser first, isn’t it now time to put the consumer first?